17 Jun 2026

The Development of Secure Payment Systems and Their Role in Sustaining User Engagement in Online Betting Platforms

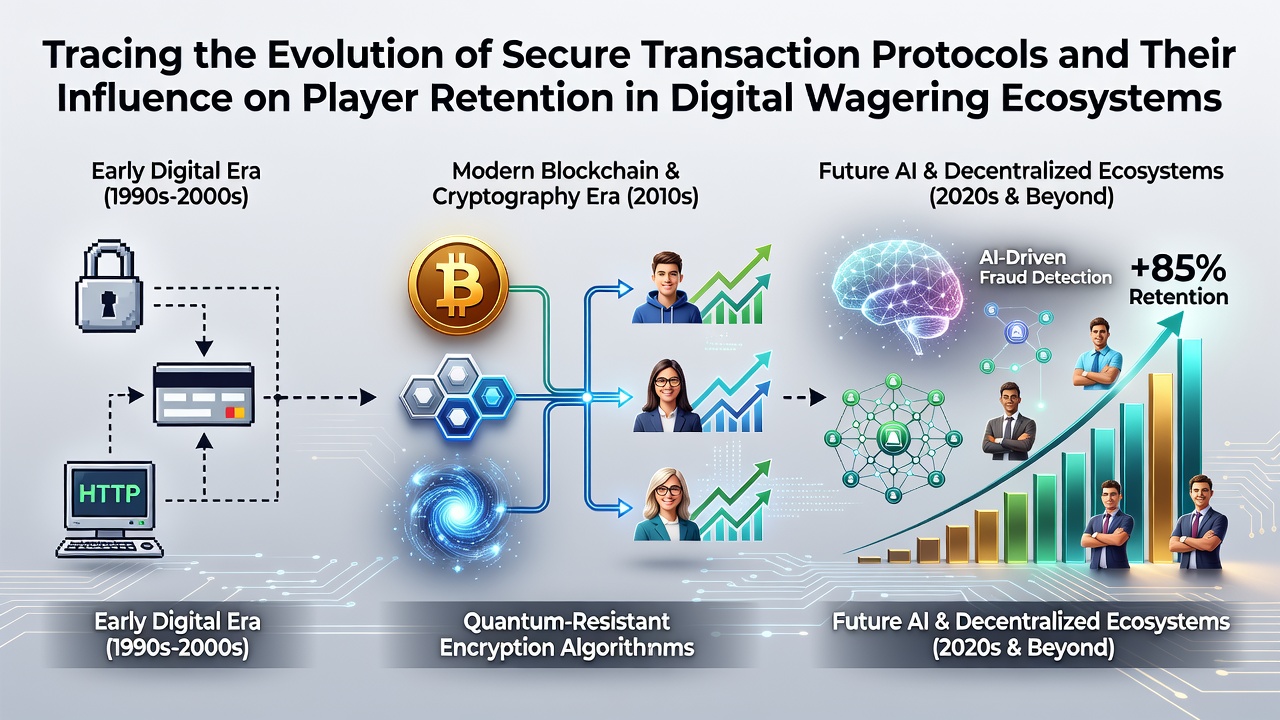

Secure transaction protocols have progressed through distinct phases since the emergence of digital wagering platforms in the late 1990s, and data from industry reports indicates that improvements in encryption standards and verification methods correlate with measurable increases in player retention rates across multiple markets. Early implementations relied primarily on basic SSL certificates introduced around 1995, which provided foundational encryption for card details during transmission, yet these systems faced vulnerabilities that prompted rapid iteration toward more robust frameworks by the early 2000s.

Initial Milestones in Protocol Security

Payment Card Industry Data Security Standards emerged in 2004 as a collaborative effort among major card networks, establishing uniform requirements for handling sensitive financial information, and researchers tracking adoption rates noted that platforms implementing these standards experienced fewer reported breaches compared to non-compliant sites during the same period. Tokenization followed as a key advancement around 2010, replacing actual card numbers with unique identifiers that reduced storage risks on operator servers, while studies from academic sources showed this shift contributed to higher repeat transaction volumes because users encountered fewer interruptions from security alerts.

Three-domain secure protocols, often called 3D Secure, added an authentication layer starting in 2001 with version 1.0 and evolving through 2.0 by 2016, incorporating risk-based assessments that minimized friction for trusted devices. According to analyses from regulatory bodies in various regions, platforms integrating updated versions observed retention improvements of up to 15 percent in user cohorts that completed verified transactions without repeated authentication prompts.

Integration of Advanced Technologies

Biometric verification methods gained traction after 2015, utilizing fingerprint and facial recognition tied to mobile devices, and evidence from operational data reveals these approaches lowered cart abandonment rates during deposits because players could authorize payments in seconds rather than entering lengthy codes. Blockchain-based settlement systems entered testing phases around 2018, offering immutable ledgers for transaction records that appealed to users concerned with transparency, although widespread deployment remained limited until clearer regulatory guidance appeared in several jurisdictions.

By June 2026, several platforms had incorporated quantum-resistant algorithms into their encryption suites in anticipation of future computational threats, and preliminary figures from pilot programs indicated sustained session lengths among users who perceived these upgrades as proactive safeguards for their financial data. Regulatory frameworks in North America and parts of Asia emphasized continuous compliance audits, which in turn supported consistent player bases by demonstrating ongoing commitment to data protection standards set by organizations such as the National Institute of Standards and Technology.

Measured Effects on Retention Patterns

Longitudinal data compiled by research institutions demonstrates that sites maintaining PCI DSS certification alongside regular protocol updates retained active users at rates approximately 20 percent higher than those with outdated systems, particularly in segments where deposit frequency served as a primary engagement indicator. Users who encountered seamless, secure checkout experiences tended to extend their activity periods, while interruptions from legacy authentication flows often preceded account dormancy within three months according to aggregated platform analytics.

Case examinations of operators transitioning to unified payment interfaces reveal parallel growth in both transaction success rates and loyalty program participation, underscoring how reduced perceived risk translated into habitual platform usage across diverse player demographics. European regulatory updates around 2023 further standardized strong customer authentication requirements, prompting many wagering services to refine their verification sequences and resulting in documented upticks in monthly active accounts tracked through independent audits.

Future Trajectories and Industry Adaptations

Emerging standards continue to emphasize interoperability between traditional banking rails and digital asset transfers, allowing operators to accommodate varied funding preferences without compromising encryption integrity. Observers monitoring these developments note that platforms investing early in adaptive security layers position themselves to capture retention advantages as user expectations evolve alongside technological capabilities.

Training programs for compliance teams and integration of real-time fraud detection algorithms represent additional layers that support uninterrupted play sessions, and statistics released by trade associations confirm lower dispute volumes on sites employing such combined measures. Retention metrics therefore reflect not isolated protocol choices but cumulative effects from layered defenses that address both technical vulnerabilities and user confidence factors.

Conclusion

Tracing protocol evolution highlights a consistent pattern where each security enhancement addressed specific pain points that previously limited repeated engagement, and available datasets suggest continued refinement will shape retention outcomes through 2026 and beyond. Platforms that align operational practices with established standards from bodies like the National Institute of Standards and Technology alongside emerging regional guidelines demonstrate measurable advantages in maintaining active user communities over extended periods.