12 Jul 2026

Tracing Funding Routes: Shifts in Deposit Methods Across Digital Wagering Eras

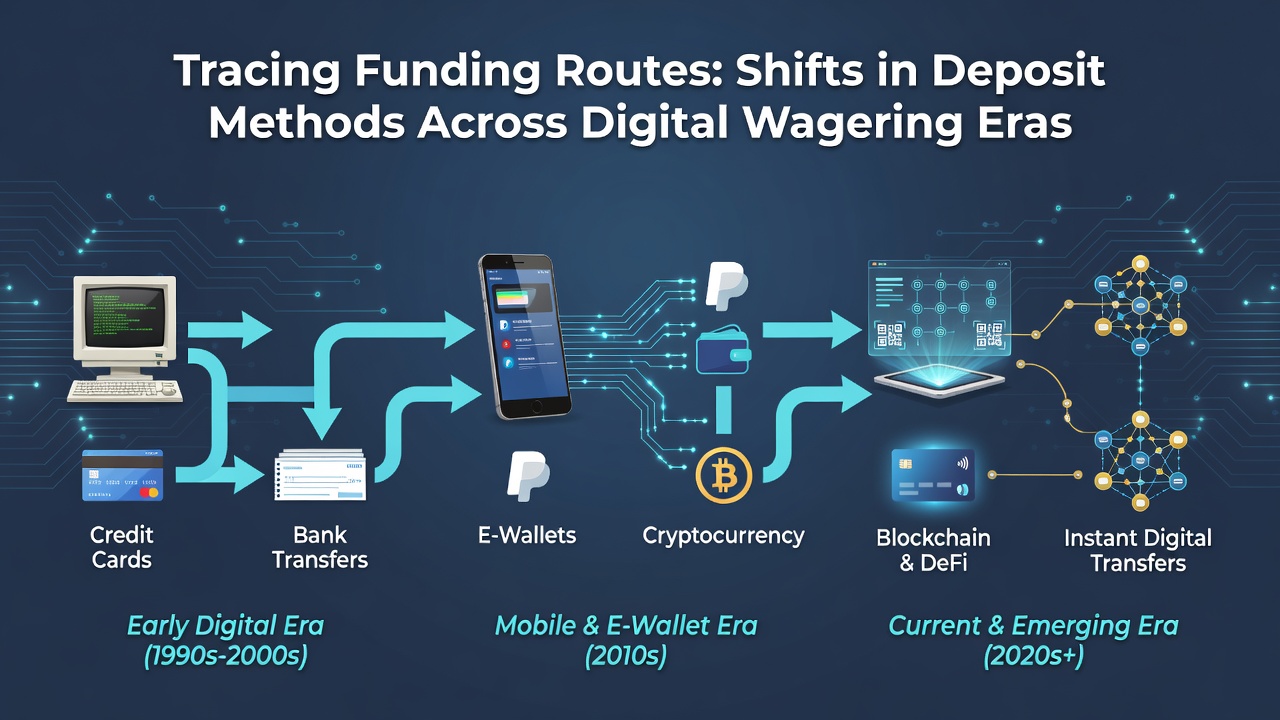

Digital wagering has seen deposit methods evolve through distinct eras shaped by technology, regulation, and consumer behavior. Observers note that early platforms relied heavily on traditional banking channels, while later periods introduced electronic intermediaries and decentralized options that altered how funds move between players and operators.

Initial Digital Wagering Period: Banking Transfers and Card Systems

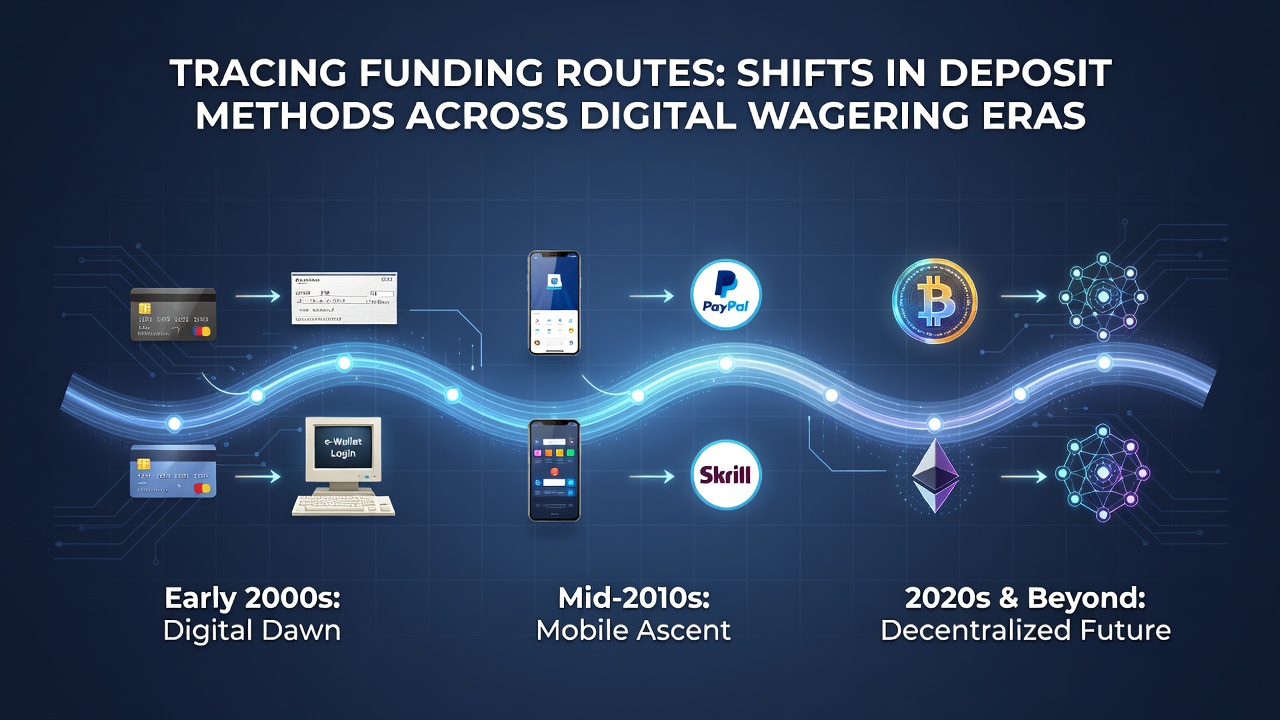

During the 1990s and early 2000s, deposit routes centered on credit cards and bank wires because these channels already existed in mainstream finance. Research from regulatory bodies indicates that credit card transactions accounted for the majority of activity in licensed markets across North America and parts of Europe at the time. Bank transfers offered higher limits but required longer processing windows that sometimes stretched into several business days. Those who studied transaction logs from that era found that operators absorbed chargeback risks as a standard cost of doing business.

Payment processors began segmenting wagering activity from other merchant categories around 2005, which forced platforms to adapt quickly. Data from industry reports shows that many sites shifted toward prepaid cards and money orders to maintain continuity when card networks tightened rules. This adjustment period highlighted how external policy decisions could redirect entire funding pathways overnight.

Expansion Phase: Electronic Wallets and Stored Value Options

Electronic wallets entered the scene as intermediaries that decoupled wagering deposits from direct bank involvement. Services such as Neteller and Skrill gained traction because they allowed faster settlement and reduced exposure to card network restrictions. According to figures compiled by Australian regulatory agencies, wallet-based deposits rose steadily between 2010 and 2015 in markets where operators accepted these methods. Users could fund wallets through local bank transfers or retail outlets, creating an additional layer that masked the final destination of funds.

Mobile carriers in several regions started offering direct billing options during this same window. Data collected by Canadian provincial authorities reveals that carrier billing captured a measurable share of smaller deposits, particularly among users without traditional banking relationships. The convenience factor proved significant, yet transaction caps and higher fees limited broader adoption. Observers tracking volume trends noted that these methods filled gaps rather than replacing established routes entirely.

Cryptocurrency Integration and Decentralized Pathways

Bitcoin and subsequent digital currencies appeared as alternative deposit routes after 2013, driven by users seeking greater privacy and lower fees. Studies published in academic journals on financial technology document an initial surge followed by volatility tied to price swings and regulatory responses. Several operators integrated crypto processors that converted deposits automatically into fiat balances, reducing friction for players unfamiliar with wallet management. Evidence from European market analyses indicates that crypto deposits grew fastest in jurisdictions where traditional channels faced licensing hurdles.

Stablecoins later emerged as a refinement because they minimized exchange rate risk while retaining blockchain settlement speed. Reports from research institutions in Asia show increased usage of these assets for cross-border deposits, particularly where currency controls complicated conventional transfers. The underlying ledger technology allowed operators to verify transactions without relying on intermediary banks, which changed compliance workflows for those accepting such methods.

Regulatory Pressures and Recent Adaptations Through July 2026

By July 2026, several jurisdictions had implemented updated verification standards that affected how deposit methods operate. Real-time identity checks became more common, requiring platforms to integrate additional layers of authentication regardless of funding source. Figures released by the New Jersey Division of Gaming Enforcement illustrate that approved payment processors must now maintain detailed audit trails for every transaction above certain thresholds. These requirements have prompted operators to consolidate partnerships with fewer, more heavily vetted providers.

Open banking frameworks in parts of Europe and Australia have enabled direct account-to-account transfers that bypass traditional card rails. Data compiled by the European Gaming and Betting Association shows that these instant bank payment options captured increasing market share during 2025 and into 2026. The shift reduced processing times to seconds while maintaining compliance visibility for regulators. Operators that adopted these systems early reported fewer declined deposits compared with legacy card routes.

Conclusion

Deposit method evolution in digital wagering reflects ongoing interplay between technological capability, regulatory oversight, and user preferences. Each era introduced new routes that addressed limitations of previous systems while creating fresh compliance considerations. Current patterns suggest continued fragmentation rather than convergence toward a single dominant channel, with operators maintaining multiple options to accommodate diverse player bases across regions.